Not exporting feeder cattle to the U.S. means that more cattle are staying in Mexico to be finished for beef production.

Derrell S. Peel, Oklahoma State University

New World Screwworm (NWS) issues and the closure of the Mexican border for livestock have focused much attention on the Mexican beef industry. Questions have continued about if and how the Mexican industry could handle the one million plus head of cattle that are typically exported to the U.S. The Mexican beef industry has evolved significantly in the past two decades, rendering many older views of the industry outdated and incorrect.

For the past 15 years, the total Mexican cattle inventory has averaged between 17 and 18 million head, with a total cow herd of roughly 11.5 million head. Cows make up a larger percentage of total cattle inventories (about 65 percent) compared to the U.S, where the total cow herd is 43 percent of total cattle. This is because cattle flow through the Mexican industry faster than in the U.S. More young cattle are typically included in the total U.S. inventory because calves remain on pasture and in feedlots, whereas 14 to 16 percent of the Mexican calf crop is usually exported and cattle do not remain in feedlots as long compared to the U.S.

The Mexican calf crop has averaged just over eight million head in recent years, with a calf crop percentage of roughly 71 percent, up from about 65 percent 25 years ago. Mexican cattle exports have averaged 1.2 million head over the last 25 years and typically represent 14 to 16 percent of the calf crop.

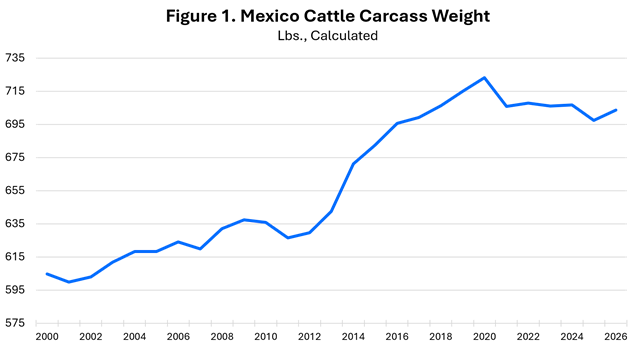

Beef production in Mexico has increased an average of two percent per year in the last decade. This is the result of increased cattle slaughter, about 1.6 percent annually, and increasing carcass weights. Average cattle carcass weights have increased from about 600 pounds twenty-five years ago to roughly 710 pounds currently. The Mexican beef industry evolved from predominantly grass-fed production to current production where most cattle are fed in feedlots. This, along with improved cattle genetics and management, has led to increased carcass weights (Figure 1).

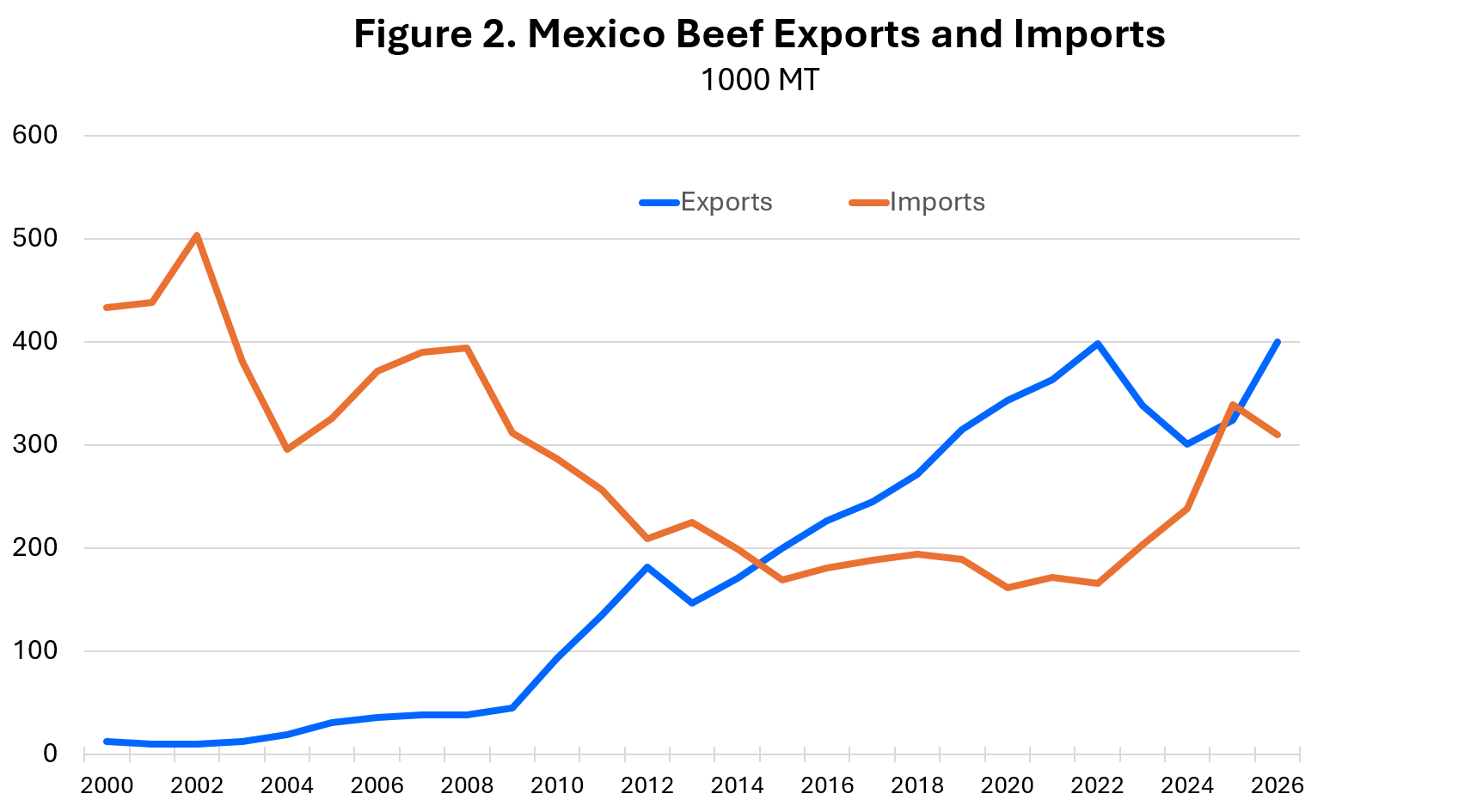

Beef consumption in Mexico averages about 24 pounds per year, retail weight. Beef imports in Mexico are equivalent to roughly ten percent of production in recent years but down from about 22 percent of production two decades ago. Moreover, Mexico has become a significant beef exporter and has been a net exporter the past ten years. (Figure 2). Mexico is currently the number eleven beef exporting country.

The Mexican beef industry has modernized and developed significant infrastructure the past two-plus decades. Cattle and beef trade between Mexico and the U.S. has evolved from a long history of cattle exports to the U.S. to include Mexico becoming a major beef export destination for the U.S., and recently with Mexico becoming a significant source of U.S. beef imports. The increasingly integrated trade relationship adds value to the beef industries in both countries.

Not exporting feeder cattle to the U.S. means that more cattle are staying in Mexico to be finished for beef production. It also likely means that fewer cattle are being imported from Central America, which has been a source of supplemental cattle supply in recent years. Mexican beef imports will likely decrease, and beef exports will increase in the absence of cattle exports. Production systems and supply chains will continue to evolve in Mexico.