The initial stages of expansion that are underway mean that cattle slaughter and beef production will continue to decline and that the highest cattle prices of this cycle are still ahead.

Derrell S. Peel, Oklahoma State University

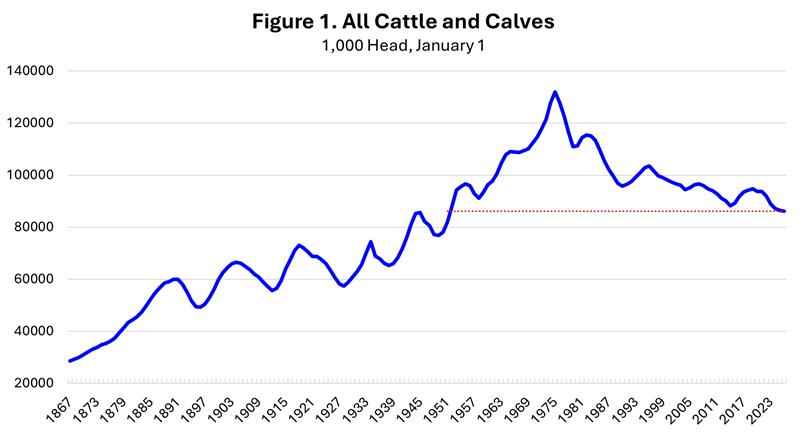

The U.S. cattle industry has been characterized by cycles of inventory and prices since the modern ranching industry developed in the late 1800s. There have been twelve cyclical inventory peaks in the last 129 years, with the first in 1890 and most recently in 2019 (Figure 1 above). Cycles have been persistent regardless of whether the inventory has been trending higher or lower.

From the current inventory low (maybe, depending on drought), the most important question in the industry is when herd rebuilding will begin. Both increased heifer retention and reduced cow culling are needed to stabilize the herd inventory at a low and begin expansion. Beef cow culling has decreased sharply since 2022, from a peak of 13.2 percent to 8.4 percent in 2025. Beef cow slaughter is down again year over year in 2026 and currently indicates a beef cow culling rate of 7.1 percent for the year, which would be a record low culling level.

The high calf prices that historically trigger heifer retention have been in place since 2023. More heifer retention means that heifer slaughter must decline. Heifer slaughter has declined in total numbers since 2022; however, it has declined little relative to total fed cattle slaughter. In other words, heifer slaughter is down simply because there are fewer cattle, but it has not declined enough to indicate substantial heifer retention. The beef replacement heifer inventory was up a scant 0.9 percent year over year on January 1, enough to suggest only the beginning of heifer retention.

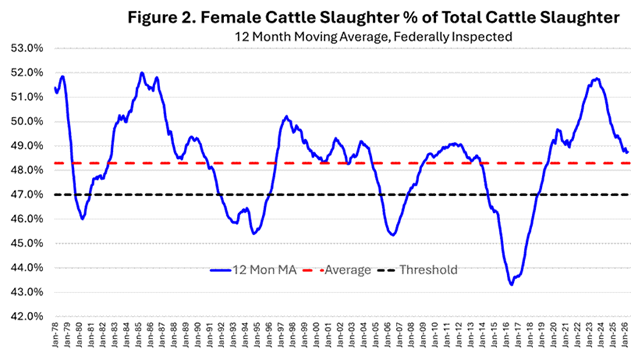

Ultimately, the best indicator of herd rebuilding is the combination of heifer and cow slaughter into total female slaughter. Figure 2 shows a twelve-month moving average of total female slaughter as a percentage of total cattle slaughter. The female slaughter percentage peaked most recently in 2023 at 51.8 percent (the highest level since 1985) and has decreased to the current level of 48.8 percent. Female cattle slaughter is still above the average level (red dashed line). Most of the decrease observed thus far in the female slaughter percentage is due to decreased beef cow slaughter. Further decreases will depend on increased heifer retention (i.e. reduced heifer slaughter).

A commonly recognized threshold for herd expansion is when the female slaughter percentage drops below 47 percent (black dashed line). Figure 2 above shows the last four cattle cycles and the female slaughter percentage that corresponded to herd rebuilding. The female slaughter percentage dropped below 47 percent from October 1979 – November 1980 (46.0 percent low); February 1992 – January 1996 (45.4 percent low); July 2005 – September 2007 (45.3 percent low); and July 2014 – August 2018 (43.3 percent low). On average, the female slaughter percentage remained below the 47 percent threshold for 35 months, ranging from 14 months to 49 months (in the most recent expansion).

The beef cattle industry is well above the threshold at this time. The decrease in the female slaughter percentage thus far are signs of the beginnings of heifer retention. However, history suggests that it might take another 6-10 months for the female slaughter percentage to drop from the current level of 48.8 percent to the 47 percent threshold and then remain there for 14 to as much as 49 months depending on the amount of herd expansion. The initial stages of this process mean that cattle slaughter and beef production will continue to decline and that the highest cattle prices of this cycle are still ahead.