Derrell S. Peel, Oklahoma State University

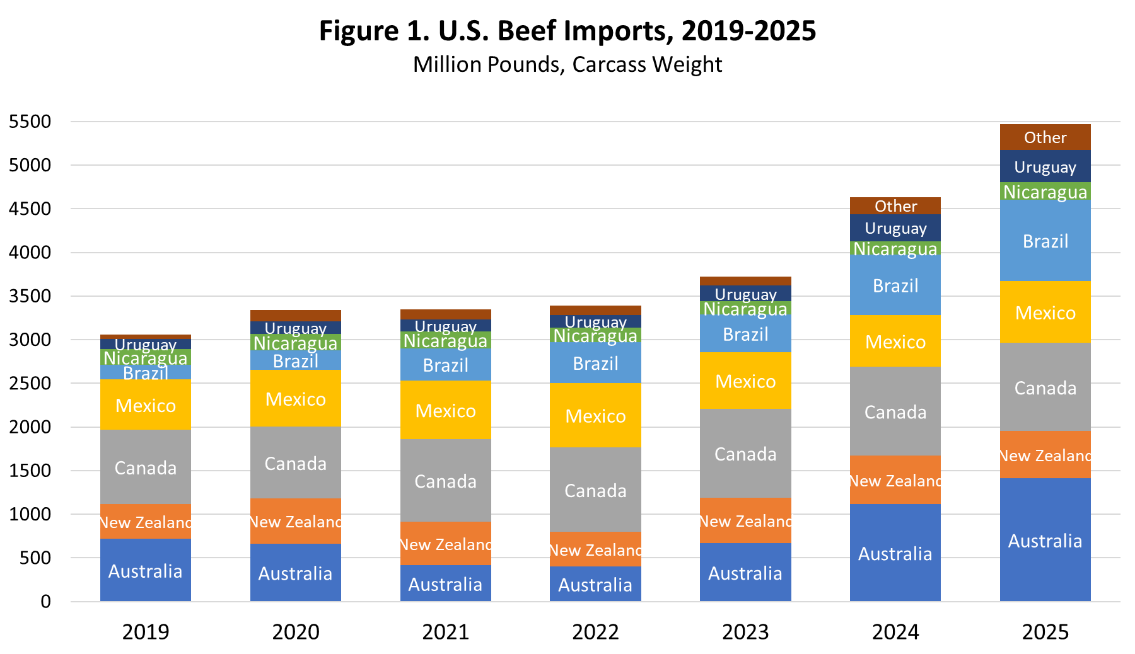

Beef imports increased 18.0 percent year over year in 2025 and are up 61.4 percent since 2022, the year of record U.S. beef production and when the current market run began. Total beef production in 2025 was down 3.6 percent year over year and is down 8.1 percent since 2022. More important relative to beef imports, production of nonfed beef (from cull cows and bulls) was down 8.0 percent last year and is down 24.8 percent since 2022. In fact, nonfed beef production in 2025 was the smallest total since 2005.

Increased beef imports are the market response to declining lean beef supplies due to decreased nonfed beef production since most beef imports are lean processing beef. Higher prices of lean beef in the U.S. prompts increased imports from any of several potential beef import sources. The amount of beef imports from various sources depends on several factors including: the country’s ability to produce and export; other export markets for the country; and relative price competitiveness of the country (which depends on exchange rates and tariffs the country faces).

Since 2022, Australia has been the largest source of beef imports (up 251.1 percent since 2022); Canada is number two (up 4.3 percent); Brazil is number three (up 99.9 percent); Mexico, number four (down 4.0 percent); number five New Zealand (up 37.2 percent); and Uruguay, number six (up 158.8 percent). Several smaller sources contributed another nine percent to total beef imports in 2025 (up 79.3 percent since 2022) (Figure 1 above).

Record high U.S. ground beef prices continue to be the focus of political discussion along with the possibility of increased beef imports to address unprecedented lean beef prices. It is important to remember that beef imports are limited only by market forces that determine the total quantity and the mix of sources supplying beef to the U.S. market. The latest data for January show some interesting changes in beef imports. Total January beef imports were up 7.7 percent year over year and up 86.0 percent compared to January 2022 (Figure 2).

Most noticeable in Figure 2 is the jump in the other category, up 119.0 percent from one year ago. The biggest part of these other sources is Paraguay, a new player in the beef import market. January beef imports from Paraguay were up 147.4 percent year over year and accounted for 61.1 percent of the other category and 10.8 percent of total monthly beef imports. Paraguay has only been exporting to the U.S. since 2024. For January, Paraguay was able to capture a significant portion of the “Other Country” quota that Brazil has dominated the past four years. January beef imports from Brazil were down 15.1 percent year over year. Combined January imports from Brazil and Paraguay were up 5.3 percent year over year. This illustrates that markets are determining the total level of imports and also the distribution of sources of beef imports.

Argentina has been the focus of much of the political discussion about beef imports. Argentina represented 26.1 percent of the other category and 2.3 percent of total beef imports in 2025 (Figure 1). Argentina has been granted an expanded tariff rate quota (TRQ) in 2026. Total beef imports from Argentina in 2025 were more than double the previous quota and were limited by market conditions rather than the quota. In January 2026, imports of Argentina were up 122.5 percent year over year but still represented just 16.1 percent of other country imports and 2.8 percent of total January imports (Figure 2). It’s not clear whether Argentina will be able to fill the additional quota this year. The increase would be at the expense of domestic consumption and/or other export markets in Argentina. Moreover, the previous discussion highlights the fact the any increase in beef imports from Argentina would likely displace some imports from other sources. Expected growth in beef imports in 2026 will continue to be determined by market forces and may include some relative increase in imports from Argentina.