Kenny Burdine… University of Kentucky

Last week’s two USDA reports were much anticipated as they provided further information about the level of beef heifer retention at the national level. Heifers, as a percentage of on-feed inventory, were estimated at 38.1% in the July Cattle-on-Feed report. This is not a number that suggests widespread retention. And the number of heifers held for beef cow replacement in the mid-year inventory report was estimated at 3.7 million head, a decrease of 100,000 heifers from July 1, 2023. I wanted to dig into that number a little deeper this week and frame it a bit with the ongoing discussion of beef cow slaughter.

I prefer to think about beef heifer retention as a percentage of beef cow inventory. A higher percentage suggests expansion of beef cow numbers is likely in the future and a smaller percentage suggests the opposite. As a percentage of estimated July 1 beef cow inventory, heifers held for beef cow replacement came in at 12.9%. That was down slightly from two years ago and is the smallest percentage in the mid-year dataset, which goes back to 1973 (see figure below). This was yet another sign that heifer retention has been very slow to develop during this cycle.

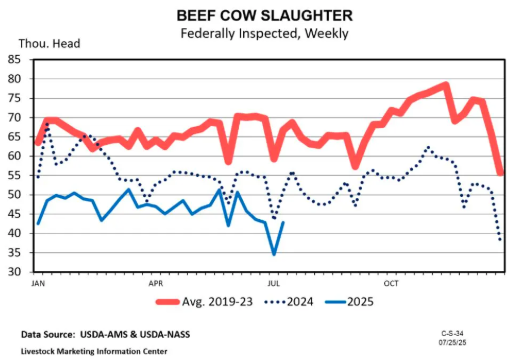

It is also important to recognize that there is some fluidity with respect to heifer development. All those heifers intended for replacement will not become cows and some heifers in the system that are not currently intended for replacement will end up getting bred. On the other hand, cow slaughter is much more definitive. Cows that have been slaughtered are gone and all that can change is the pace of beef cow slaughter going forward. Through the first six months of 2025, beef cow slaughter was down by more than 17% from the first six months of 2024. If that trend continues through the end of this year, nearly 500,000 fewer beef cows would be slaughtered in 2025.

As I write this in early August, there is still a lot of time left in 2025 and potential still exists for the pace of beef cow slaughter to increase. Up to this point, data suggests that cow-calf operators have generally been holding on to cows longer and selling heifers calves. However, cull cow prices continue to be strong and are attempting to pull more cows into the beef system. Since the majority of cow-calf operations calve in the spring and wean calves in the fall, the rest of this year will be interesting to watch for beef cow harvest patterns. I continue to expect a slight increase in beef cow inventory to start 2026, but how significant that increase is, will be determined by the pace of beef cow slaughter for the balance of 2025.