Derrell S. Peel, Oklahoma State University

The latest Cattle on Feed report showed that feedlot inventories on November 1 were 11.99 million head, equal to one year ago. Feedlot inventories have been about equal to the previous year for each of the past 14 months. October feedlot placements were 105.3 percent of year ago levels, slightly higher than pre-report expectations. Placements in October were likely enhanced by early movement of feeder cattle in October. In Oklahoma, October auction volumes were up by 45.2 percent over year earlier levels. Auction volumes dropped sharply in November. The larger, earlier fall run of calves likely means that auction volumes will be smaller for the remainder of the year. Total feedlot placements this year have been 1.1 percent less year over year.

Feedlot marketings in October were 104.7 percent of last year. However, October 2024 had one additional business day compared to last year so daily average feedlot marketings were equal to one year ago. Total feedlot marketings this year have been down slightly, just 0.1 percent less than last year.

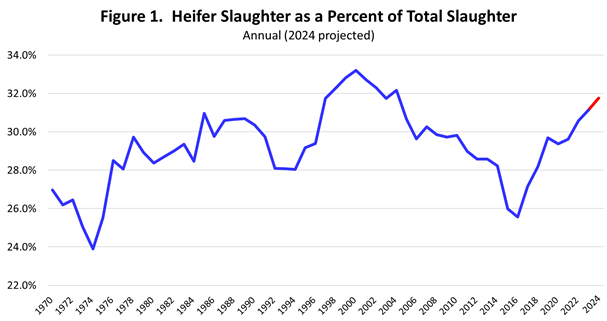

Recent slaughter data for October showed that heifer slaughter was 32.5 percent of total cattle slaughter for the month. The twelve-month moving average of heifer slaughter was 31.8 percent of total slaughter for the past year. With just two months of data left in 2024, this is a good estimate of the annual value of heifer slaughter as a percent of total cattle slaughter. This estimate is included in Figure 1 (shown in red) and shows that heifer slaughter rates continue to increase. The 2024 heifer percentage of total cattle slaughter is likely to be the highest level since 2004.

Cattle cycle herd dynamics depend on the dynamics of female cattle including both cull cows and heifers. Declining cull cow rates is often the leading indicator of producer herd rebuilding intentions. Beef cow slaughter is down 17.9 percent year over year in the first 45 weeks of 2024. This is projected to result in an annual culling rate of about ten percent, roughly equal to the long-term average and down from the recent high over 13 percent in 2022. During herd expansion the cow culling rate typically drops below nine percent for 3-4 years.

The biggest component of herd expansion is heifer retention. The heifer slaughter rates in Figure 1 above indicate that no heifer retention is occurring yet. Heifer retention usually lags changes in cow culling. Herd expansion results in decreased heifer slaughter rates similar to the 1991-1996 and the 2014-2017 periods. Current heifer slaughter rates suggest that the beef cow has continued to decrease in 2024 and that prospects for herd expansion in 2025 are very limited.