Steiner Consulting Group

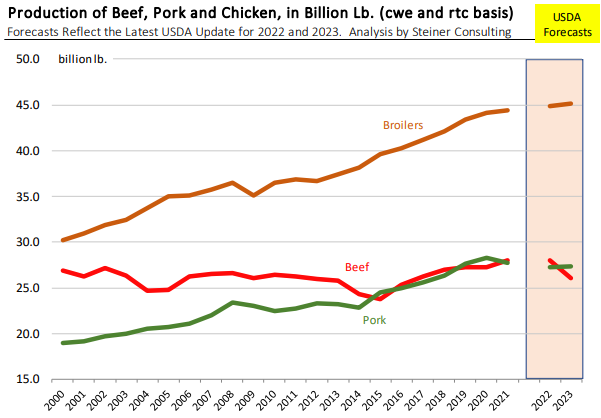

We did not provide much coverage of the latest USDA supply/demand report because USDA did not make any significant changes to its projections for 2023. But there are a lot of questions about meat protein supplies going forward and we thought putting current projections in a historical perspective may be useful. If we could summarize the broader trends in one sentence it would be: expect less beef supply, expect steady pork supplies and expect chicken to continue to grind higher. As the chart to the right shows, that has largely been the story of the past +20 years. USDA is now forecasting beef production for 2023 to be just a little over 26 billion pounds. If that forecast is realized, it would represent a reduction of about 2 billion pounds (-7%) compared to the supply of beef produced in 2021 and 2022. It also means that beef will drop to third place in terms of volume produced, behind broilers and pork.

The number of cows coming to market has yet to slow down. On Wednesday USDA reported some 30k cows and bulls coming to market and probably the same number on Thursday and for the week we think cow slaughter will be up as much as 4% from last year. Ongoing beef cow herd liquidation adds to the supply of beef produced this year while widening the shortfall in supply in future years. It’s a safe bet that we will see less beef produced in 2024 and 2025. Per capita beef consumption for 2023 is projected at 55.1 pounds per person, approaching the lows that we saw in 2014-15. If beef production continues to decline in 2024 and 2025, as we think is reasonable to expect, per capita beef consumption & availability will likely match previous lows and higher prices may be needed to ration out supply.