Kenny Burdine, University of Kentucky | Jan 12, 2022

From my perspective, cow-calf operators have been as frustrated over the last couple of years as I have ever seen them. Several commodity markets improved a great deal during 2021, but the improvement in calf prices was pretty minimal. In reality, the cow-calf sector has been handed 4-5 consecutive challenging years. Fundamentals appeared to be setting up for price improvement two years ago, but between COVID in 2020 and sharply higher grain prices in 2021, calf markets have struggled to gain any traction at all. I remain bullish on the 2022 market and think we will see our best spring calf market since 2016, but unknowns always exist. So, I wanted to focus this week’s discussion on three key questions that I think will drive this year’s calf market.

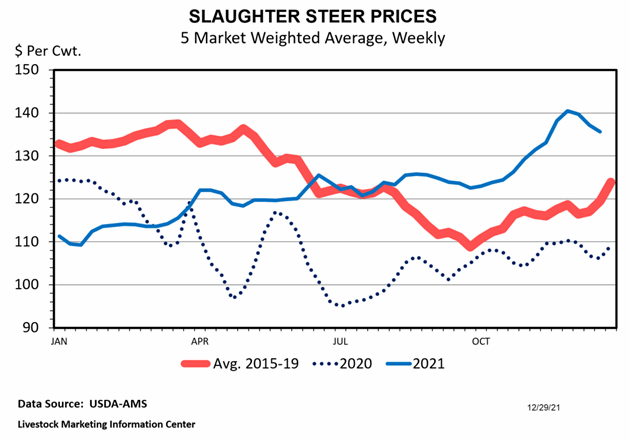

How high will fed cattle prices go?

Fed cattle prices typically make their highs in the spring of the year and move downward through summer and fall. Last year, slaughter cattle prices improved by about $17 per cwt from early October to early December, but did pull back a bit as we moved through December. As I write this on the morning of January 10th, April CME© Live Cattle futures are on the board above $140 and the break to the June contract is relatively small. Expectations of fed cattle prices drove heavy feeder values last fall and the prices levels that are actually reached this spring will set the tone for much of 2022.

What can we expect from feed prices?

Focus in the grain markets has already turned to likely 2022 production levels. The size of the South American crop is being discussed as we speak and the next couple months will be crucial as US farmers make planting decisions for the current year. There has been a lot of talk lately about fertilizer prices, but new crop corn is on the board in the mid-$5’s. Planting decisions are the starting point for estimating the size of the next crop. In addition to the typical weather / yield impact on price, it will be very interesting to see if export levels continue at the brisk pace that has been seen recently.

How much more culling will we see of the cowherd?

There is no question that this beef cow herd is smaller now than it was one year ago. The only question is, how much smaller is it? The West and the Northern Plains were dealing with drought most all of last year, while conditions in the Southern Plains turned drier in the fourth quarter. Dry conditions were definitely a factor behind the cow slaughter levels of 2021, but disappointing calf markets were also at play. It’s difficult to track cow numbers by region throughout the year, but cows appeared to be moving in regions that were not dealing with drought. I expect another decrease in beef cow numbers during 2022, and if dry conditions persist, that decrease will get even larger.

Josh ended last week’s article by mentioning that the first of the year is a good time to consider risk management strategies. There is no way to know with certainty what feeder cattle price levels will be this summer and fall. But as I write this article, August through November feeder cattle futures are all trading above $180 per cwt. It has been some time since the market has offered that type of pricing opportunity.